Good Debt vs Bad Debt: What Every Nigerian Business Owner Must Know

Let’s be honest.

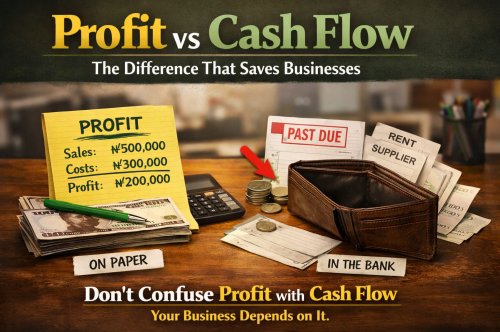

Most Nigerian business owners are not struggling because of low sales.

They are struggling because they borrow badly.

Not small mistakes. Costly ones.

They take loans that don’t return money.

They spend borrowed funds on things that don’t produce income.

Then they wonder why the business is always under pressure.

Debt is not the problem.

Wrong debt is.

If you don’t fix this, your business will keep working hard and still stay broke.

The Real Problem

Look at how most people use loans:

They borrow for weddings, birthdays, and social pressure.

They borrow to upgrade phones and lifestyle.

They borrow to “look successful” before they actually are.

Let’s call it what it is.

That is financial self-sabotage.

The money disappears fast. The repayment stays long.

Now your business is forced to carry a burden it did not create.

That is bad debt.

Bad debt does not destroy you immediately.

It drains you slowly.

- Your profit starts going into repayments

- You delay restocking because cash is tight

- You miss real opportunities because you’re already owing

- It increases Stress.

Before long, the business looks active, but nothing is growing.

You are working, but you are not moving forward.

Good Debt

Good debt is not comfortable.

It feels risky. It requires thinking. It forces discipline.

But it does one thing bad debt never does.

It pays you back.

Good debt is used to:

- Buy inventory you can sell quickly

- Invest in equipment that increases output

- Expand into opportunities with proven demand

Here’s the difference in mindset:

Bad debt consumes.

Good debt produces.

If the money you borrow cannot clearly bring back more money, you are not borrowing. You are leaking

So Before you take any loan, force yourself to answer this:

- How exactly will this money return profit?

If you cannot explain it clearly, don’t borrow. - What is the worst-case scenario?

If sales slow down, can you still survive repayments? - Is this business-driven or ego-driven?

Be honest. Many “business expenses” are just lifestyle in disguise.

If you avoid these questions, you will pay for it later.

Why Most People Still Get It Wrong is Because they borrow based on emotion, not numbers.

They assume future sales will fix today’s bad decisions.

They mix personal needs with business money.

And the biggest mistake:

They don’t build a track record.

No proof. No structure. No credibility.

So even when a real opportunity comes, they either:

- Can’t access funding

- Or only get expensive loans that kill their margins

This Is Where Most Businesses Lose the Game

Not at the beginning.

But at the moment when growth requires capital and they are not ready.

So What do Smart Operators Do Differently?

They don’t rush into loans.

They build first.

They:

- Start with what they have

- Reinvest profits consistently

- Track every transaction

- Build relationships with real buyers and suppliers

So when they finally borrow, it’s not hope.

It’s calculated.

When you use platforms like Tarevisos to deal with verified buyers and suppliers, you’re not just trading.

You’re building proof.

Every transaction becomes evidence that:

- Your business is active

- Your cash flow is real

- You are reliable

That is what lenders trust.

Not your promises. Your history.

So, If your business cannot survive without a loan, the problem is not capital.

It is structure.

Fix your operations first.

Then use debt to accelerate, not to rescue.

A Rule You Should Never Break

Borrow to grow.

Never borrow to impress.

One builds your future.

The other destroys it quietly.

Start Small. Move Smart